The acquisition and value creation playbook

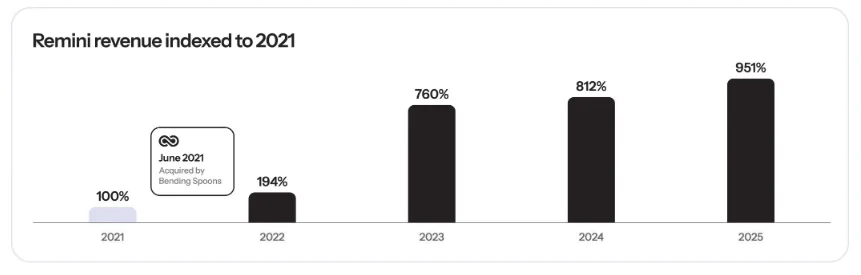

Remini is the clearest blowout success: a 2021 acquisition that became a much larger product by 2025.

Target screen

$50M-$5B of revenue, subscription or advertising model, high retention, low paid-ad dependence, manageable AI risk, and room to improve.

Underwriting

Debate assumption distributions, run Monte Carlo IRR and NPV, with discipline to walk away if price doesn't hit hurdles.

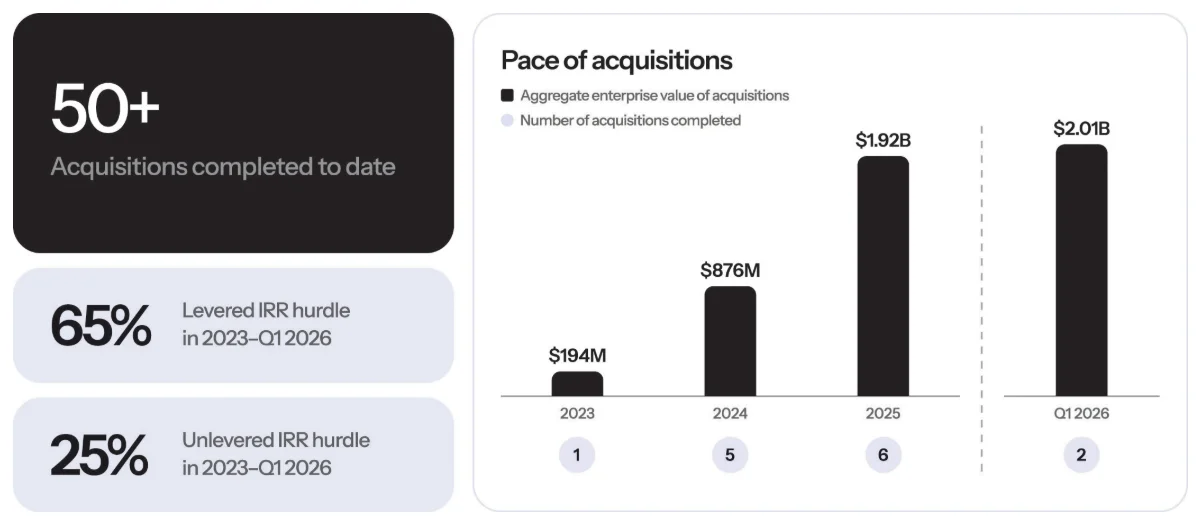

Recent hurdles: 65% levered IRR and 25% unlevered IRR.

Post-close

Bending Spoons says post-acquisition growth was driven by a ground-up rebuild: simplifying around core photo enhancement, launching AI image features that created viral spikes, and shifting monetization toward subscriptions.

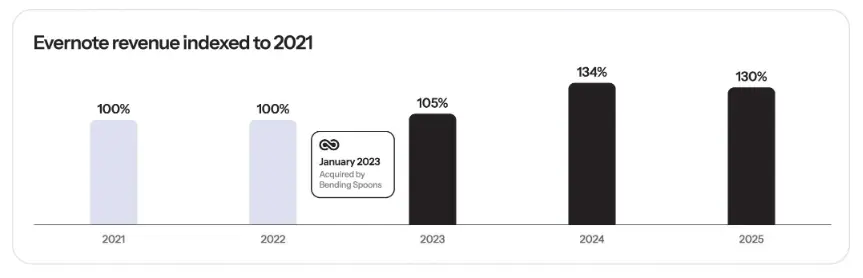

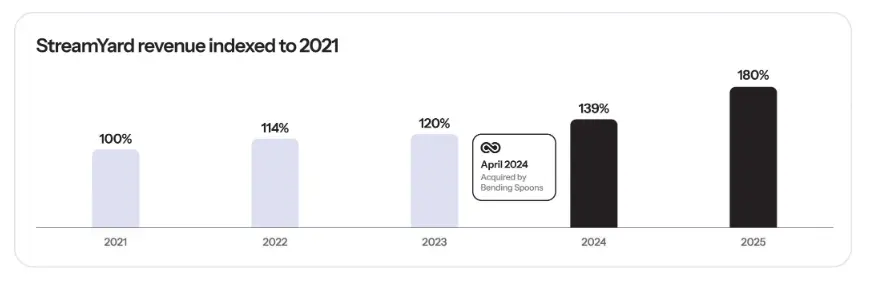

The best proof point: Acquired products have grown organically

Evernote stabilized and improved after acquisition, but growth involved higher average revenue per subscriber partly offset by fewer subscribers.

StreamYard grew revenue after acquisition driven by both subscriber growth and higher average revenue per subscriber.

Revenue acquisition mechanisms

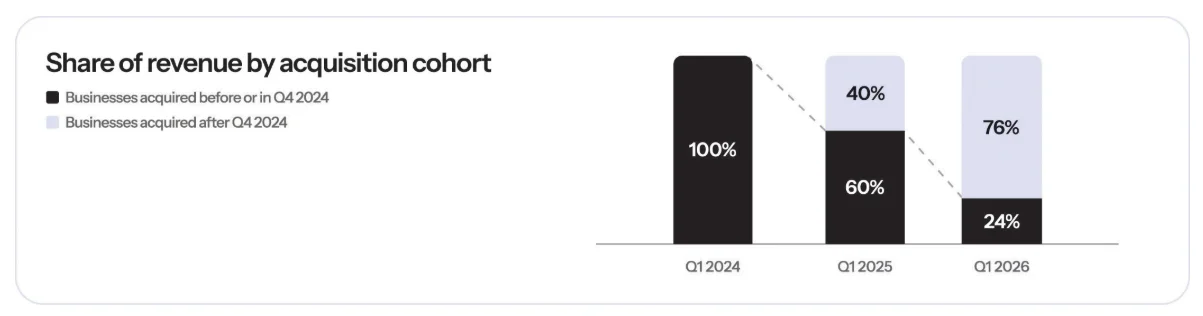

Company-level growth is acquisition-driven, but new-customer revenue within the products is still mostly organic.

Businesses that made up all Q1 2024 revenue were only 24% of Q1 2026 revenue. The old cohort grew in dollars, but new deals dominate the mix.

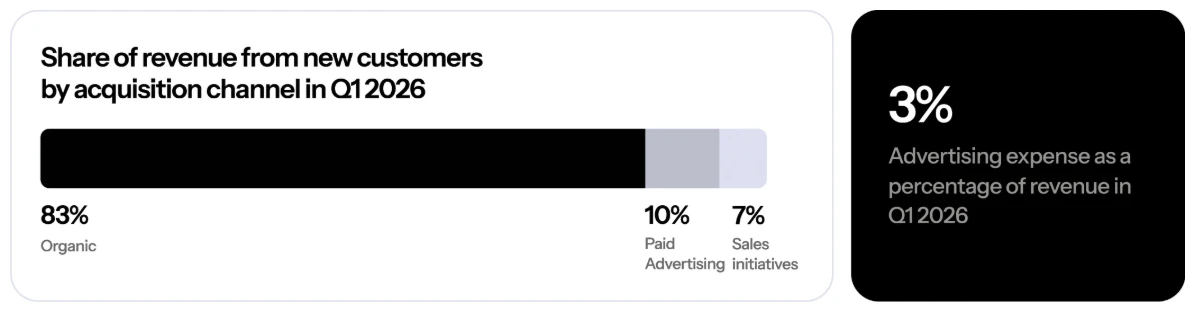

83% of Q1 2026 revenue from new customers came through organic channels, while advertising expense fell to 3% of revenue.

Debate 2: Will returns hold as deal size increases?

Three deals totaling roughly $3.3B in five months test whether Bending Spoons' historic returns hold at scale.

Bull case

Bigger #1 or #2 brands can be more efficient when transformation effort does not scale linearly with revenue.

Bear case

Bending Spoons is taking on execution, integration, AI, and leverage risk, together.

Runway

The target list exceeds 1,000 digital businesses, representing nearly $400B of aggregate estimated 2025 revenue.

Culture, governance, and management

A talent-led model with unusual equity participation

- Talent as product About 800K applications for 286 hires in 2025; Bending Spoons emphasizes lean teams and high talent density.

- Equity alignment 84% of eligible team members chose to convert part of cash salary into stock options in 2025.

- Regulatory overhang CFIUS reviews for AOL and Eventbrite could restrict integration and directly interfere with the playbook.